Forces At Work In Changing Financial Services

The Forces Accelerating Change in Financial Services

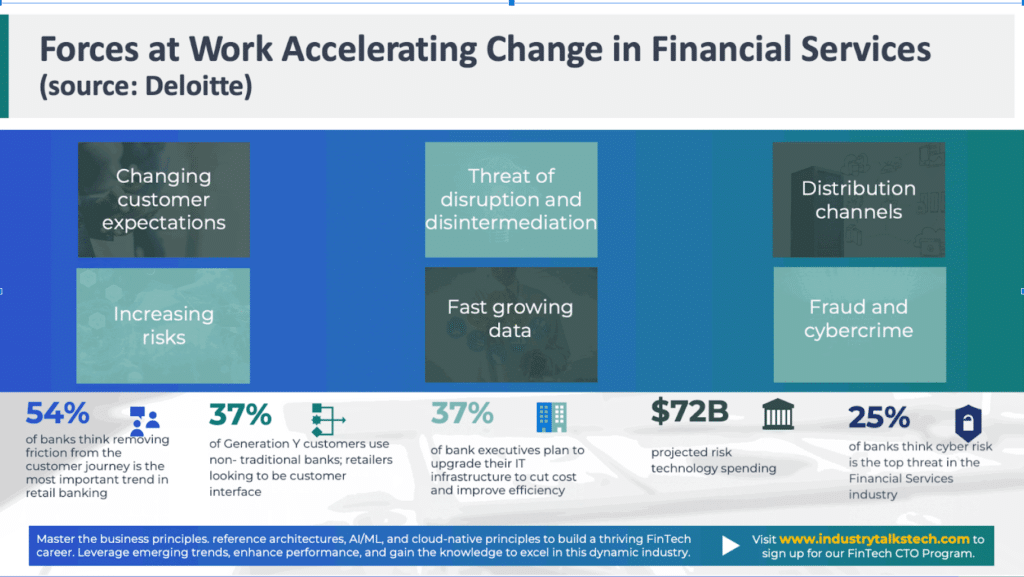

The financial services industry, once known for its physical branch networks and paper statements, is shedding its traditional skin at lightning speed. Post Covid, a confluence of powerful forces is driving change at an unprecedented pace, forcing established players to adapt or risk becoming disintermediated. In this blog, we’ll explore six key trends reshaping the landscape, using real-world examples to illustrate their impact:

1. Changing Consumer Tastes: Remember the last time you visited a physical bank branch? For many, it’s been ages. Gone are the days of waiting in line for a teller – consumers today demand the convenience and personalization of mobile banking apps like Robinhood and Chime, which offer fractional stock investing and budget-friendly features tailored to millennials and Gen Z.

2. Threat of Disruption and Disintermediation: Remember the video giant Blockbuster and their fate in the face of a digital Netflix? Fintech startups like Klarna are eating into the credit card market with “buy now, pay later” options, while Wealthfront and Betterment are challenging traditional wealth management giants with low-cost, robo-advisor services. The threat is real, and established players need to innovate like JPMorgan Chase with their Finn AI-powered chatbot or Citibank with their digital-first banking experience.

3. Distribution Channels in Flux: Branch closures are becoming commonplace as mobile banking adoption soars. Bank of America, for example, plans to close 300 branches by 2023, focusing instead on investing in their mobile app and online platform. Physical branches aren’t dead, but they’re evolving into experience centers offering financial services advice and personalized consultations, like HSBC’s innovation hubs.

4. Increasing Risks: Remember the 2008 financial crisis? No one wants a repeat. Today, institutions like Barclays are leveraging AI to proactively identify and manage risks associated with climate change, while HSBC uses advanced analytics to detect fraudulent transactions in real-time. It’s not just about reacting to risks anymore, but anticipating and mitigating them.

5. Fast-Growing Data: Every swipe, click, and transaction generates data. Capital One analyzes anonymized customer data to identify spending patterns and offer personalized budgeting tools, while DBS Bank in Singapore uses AI to provide customers with real-time insights into their financial health. Data is the new gold, but harnessing it responsibly is key.

6. Fraud & Cybercrime on the Rise: As one saw in the massive Equifax data breach in 2017, Cybercriminals are constantly evolving, and financial services institutions need to be one step ahead. Bank of Montreal leverages machine learning to detect and prevent unauthorized access to customer accounts, while Standard Chartered invests heavily in cybersecurity training and awareness programs for employees. Vigilance is crucial in today’s digital landscape.

We take the position that these forces are not just challenges, but also opportunities. By embracing them, financial institutions can develop innovative products like Nubank’s credit card with instant rewards or Ally Bank’s interest-free overdraft protection. They can improve operational efficiency like ING Bank’s automated loan approval process or JPMorgan Chase’s blockchain-based trade finance platform. And they can build stronger relationships with their customers like Chase Sapphire’s loyalty program or Wells Fargo’s financial education initiatives.

The future of financial services is unpredictable, but one thing is certain: change is here to stay. By understanding the forces driving this change and proactively adapting, financial institutions can not only survive but thrive in this dynamic new landscape. Is your business model ready for the ride? And more importantly your platform architecture?

For more information, visit “Fintech CTO Training” or contact us.